Backtesting

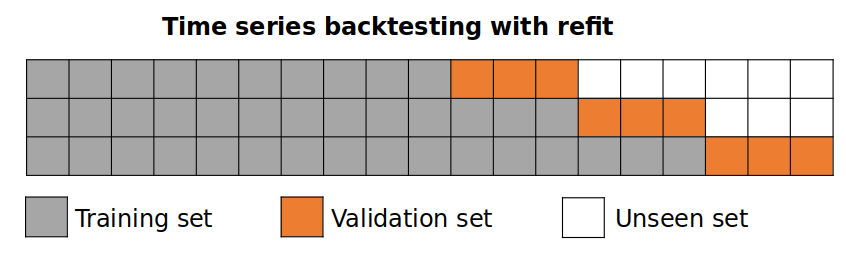

Backtesting with refit

The model is trained each tieme before making the predictions, in this way, the model use all the information available so far. It is a variation of the standar cross-validation but, instead of making a random distribution of the observations, the training set is increased sequentially, maintaining the temporal order of the data.

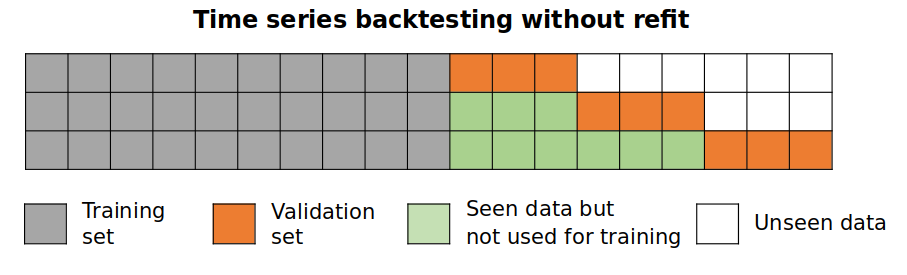

Backtesting without refit

After an initial train, the model is used sequentially without updating it and following the temporal order of the data. This strategy has the advantage of being much faster since the model is only trained once. However, the model does not incorporate the latest information available so it may lose predictive capacity over time.

Libraries

# Libraries

# ==============================================================================

import numpy as np

import pandas as pd

import matplotlib.pyplot as plt

from skforecast.ForecasterAutoreg import ForecasterAutoreg

from skforecast.model_selection import backtesting_forecaster

from sklearn.linear_model import Ridge

from sklearn.metrics import mean_squared_error

Data

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19 # Download data

# ==============================================================================

url = ( 'https://raw.githubusercontent.com/JoaquinAmatRodrigo/skforecast/master/data/h2o.csv' )

data = pd . read_csv ( url , sep = ',' )

# Data preprocessing

# ==============================================================================

data [ 'fecha' ] = pd . to_datetime ( data [ 'fecha' ], format = '%Y/%m/ %d ' )

data = data . set_index ( 'fecha' )

data = data . rename ( columns = { 'x' : 'y' })

data = data . asfreq ( 'MS' )

data = data [ 'y' ]

data = data . sort_index ()

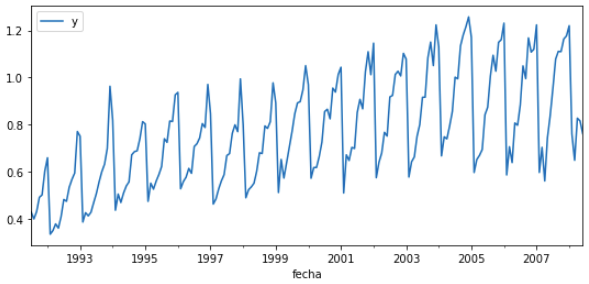

# Plot

# ==============================================================================

fig , ax = plt . subplots ( figsize = ( 9 , 4 ))

data . plot ( ax = ax )

ax . legend ()

Backtest

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20 # Backtest forecaster

# ==============================================================================

n_backtest = 36 * 3 # Last 9 years are used for backtest

data_train = data [: - n_backtest ]

data_test = data [ - n_backtest :]

forecaster = ForecasterAutoreg (

regressor = RandomForestRegressor ( random_state = 123 ),

lags = 15

)

metric , predictions_backtest = backtesting_forecaster (

forecaster = forecaster ,

y = data ,

initial_train_size = len ( data_train ),

steps = 10 ,

metric = 'mean_squared_error' ,

refit = True ,

verbose = True

)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41 Information of backtesting process

----------------------------------

Number of observations used for initial training: 96

Number of observations used for backtesting: 108

Number of folds: 11

Number of steps per fold: 10

Last fold only includes 8 observations.

Data partition in fold: 0

Training: 1991-07-01 00:00:00 -- 1999-06-01 00:00:00

Validation: 1999-07-01 00:00:00 -- 2000-04-01 00:00:00

Data partition in fold: 1

Training: 1991-07-01 00:00:00 -- 2000-04-01 00:00:00

Validation: 2000-05-01 00:00:00 -- 2001-02-01 00:00:00

Data partition in fold: 2

Training: 1991-07-01 00:00:00 -- 2001-02-01 00:00:00

Validation: 2001-03-01 00:00:00 -- 2001-12-01 00:00:00

Data partition in fold: 3

Training: 1991-07-01 00:00:00 -- 2001-12-01 00:00:00

Validation: 2002-01-01 00:00:00 -- 2002-10-01 00:00:00

Data partition in fold: 4

Training: 1991-07-01 00:00:00 -- 2002-10-01 00:00:00

Validation: 2002-11-01 00:00:00 -- 2003-08-01 00:00:00

Data partition in fold: 5

Training: 1991-07-01 00:00:00 -- 2003-08-01 00:00:00

Validation: 2003-09-01 00:00:00 -- 2004-06-01 00:00:00

Data partition in fold: 6

Training: 1991-07-01 00:00:00 -- 2004-06-01 00:00:00

Validation: 2004-07-01 00:00:00 -- 2005-04-01 00:00:00

Data partition in fold: 7

Training: 1991-07-01 00:00:00 -- 2005-04-01 00:00:00

Validation: 2005-05-01 00:00:00 -- 2006-02-01 00:00:00

Data partition in fold: 8

Training: 1991-07-01 00:00:00 -- 2006-02-01 00:00:00

Validation: 2006-03-01 00:00:00 -- 2006-12-01 00:00:00

Data partition in fold: 9

Training: 1991-07-01 00:00:00 -- 2006-12-01 00:00:00

Validation: 2007-01-01 00:00:00 -- 2007-10-01 00:00:00

Data partition in fold: 10

Training: 1991-07-01 00:00:00 -- 2007-10-01 00:00:00

Validation: 2007-11-01 00:00:00 -- 2008-06-01 00:00:00

print ( f "Error de backtest: { metric } " )

Error de backtest: [0.00726621]

predictions_backtest . head ( 4 )

| | pred |

|:--------------------|---------:|

| 1999-07-01 00:00:00 | 0.712336 |

| 1999-08-01 00:00:00 | 0.750542 |

| 1999-09-01 00:00:00 | 0.802371 |

| 1999-10-01 00:00:00 | 0.806941 |

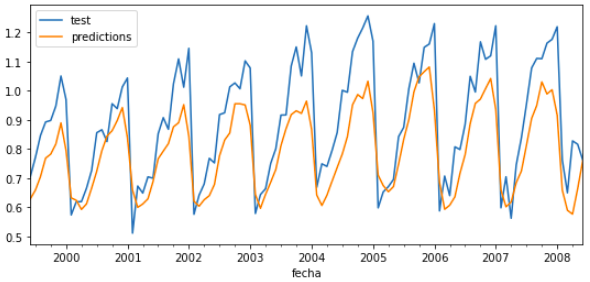

# Plot backtest predictions

# ==============================================================================

fig , ax = plt . subplots ( figsize = ( 9 , 4 ))

data_test . plot ( ax = ax , label = 'test' )

predictions_backtest . plot ( ax = ax , label = 'predictions' )

ax . legend ();

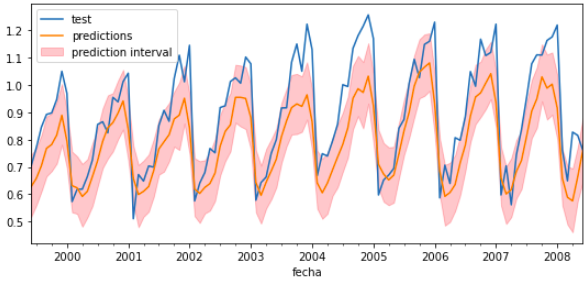

Backtest with prediction intervals

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22 # Backtest forecaster

# ==============================================================================

n_backtest = 36 * 3

data_train = data [: - n_backtest ]

data_test = data [ - n_backtest :]

forecaster = ForecasterAutoreg (

regressor = Ridge (),

lags = 15

)

metric , predictions_backtest = backtesting_forecaster (

forecaster = forecaster ,

y = data ,

initial_train_size = len ( data_train ),

steps = 10 ,

metric = 'mean_squared_error' ,

refit = True ,

interval = [ 5 , 95 ],

n_boot = 500 ,

verbose = True

)

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38

39

40

41 Information of backtesting process

----------------------------------

Number of observations used for initial training: 96

Number of observations used for backtesting: 108

Number of folds: 11

Number of steps per fold: 10

Last fold only includes 8 observations.

Data partition in fold: 0

Training: 1991-07-01 00:00:00 -- 1999-06-01 00:00:00

Validation: 1999-07-01 00:00:00 -- 2000-04-01 00:00:00

Data partition in fold: 1

Training: 1991-07-01 00:00:00 -- 2000-04-01 00:00:00

Validation: 2000-05-01 00:00:00 -- 2001-02-01 00:00:00

Data partition in fold: 2

Training: 1991-07-01 00:00:00 -- 2001-02-01 00:00:00

Validation: 2001-03-01 00:00:00 -- 2001-12-01 00:00:00

Data partition in fold: 3

Training: 1991-07-01 00:00:00 -- 2001-12-01 00:00:00

Validation: 2002-01-01 00:00:00 -- 2002-10-01 00:00:00

Data partition in fold: 4

Training: 1991-07-01 00:00:00 -- 2002-10-01 00:00:00

Validation: 2002-11-01 00:00:00 -- 2003-08-01 00:00:00

Data partition in fold: 5

Training: 1991-07-01 00:00:00 -- 2003-08-01 00:00:00

Validation: 2003-09-01 00:00:00 -- 2004-06-01 00:00:00

Data partition in fold: 6

Training: 1991-07-01 00:00:00 -- 2004-06-01 00:00:00

Validation: 2004-07-01 00:00:00 -- 2005-04-01 00:00:00

Data partition in fold: 7

Training: 1991-07-01 00:00:00 -- 2005-04-01 00:00:00

Validation: 2005-05-01 00:00:00 -- 2006-02-01 00:00:00

Data partition in fold: 8

Training: 1991-07-01 00:00:00 -- 2006-02-01 00:00:00

Validation: 2006-03-01 00:00:00 -- 2006-12-01 00:00:00

Data partition in fold: 9

Training: 1991-07-01 00:00:00 -- 2006-12-01 00:00:00

Validation: 2007-01-01 00:00:00 -- 2007-10-01 00:00:00

Data partition in fold: 10

Training: 1991-07-01 00:00:00 -- 2007-10-01 00:00:00

Validation: 2007-11-01 00:00:00 -- 2008-06-01 00:00:00

1

2

3

4

5

6

7

8

9

10

11

12

13

14 # Plot backtest predictions

# ==============================================================================

fig , ax = plt . subplots ( figsize = ( 9 , 4 ))

data_test . plot ( ax = ax , label = 'test' )

predictions_backtest . iloc [:, 0 ] . plot ( ax = ax , label = 'predictions' )

ax . fill_between (

predictions_backtest . index ,

predictions_backtest . iloc [:, 1 ],

predictions_backtest . iloc [:, 2 ],

color = 'red' ,

alpha = 0.2 ,

label = 'prediction interval'

)

ax . legend ();