Backtesting¶

In time series forecasting, the process of backtesting consists of evaluating the performance of a predictive model by applying it retrospectively to historical data. Therefore, it is a special type of cross-validation applied to the previous period(s).

The purpose of backtesting is to evaluate the accuracy and effectiveness of a model and identify any potential issues or areas of improvement. By testing the model on historical data, one can assess how well it performs on data that it has not seen before. This is an important step in the modeling process, as it helps to ensure that the model is robust and reliable.

Backtesting can be done using a variety of techniques, such as simple train-test splits or more sophisticated methods like rolling windows or expanding windows. The choice of method depends on the specific needs of the analysis and the characteristics of the time series data.

Overall, backtesting is an essential step in the development of a time series forecasting model. By rigorously testing the model on historical data, one can improve its accuracy and ensure that it is effective at predicting future values of the time series.

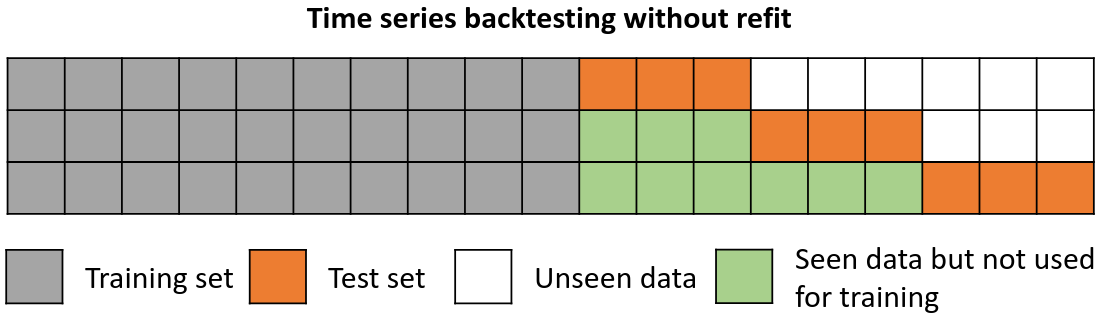

Backtesting without refit¶

Backtesting without refit is a strategy where the model is trained only once and used sequentially without updating it, following the temporal order of the data. This approach is advantageous as it is much faster than other methods that require retraining the model each time. However, the model may lose its predictive power over time as it does not incorporate the latest information available.

Backtesting without refit.

Note: The argument needed to achieve this configuration is refit=False.

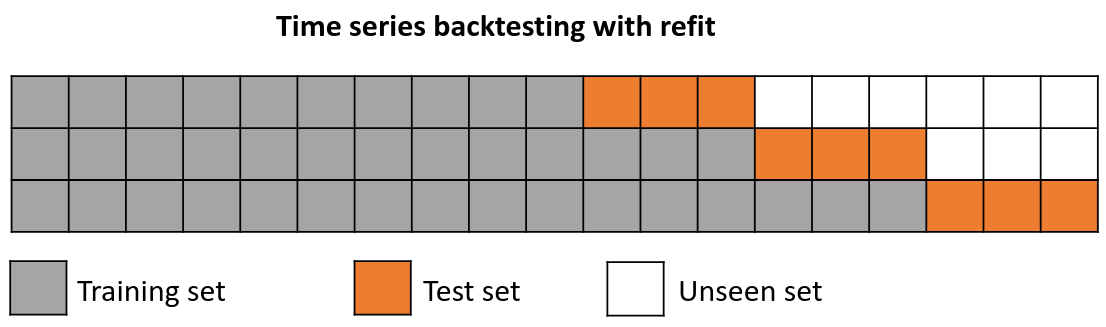

Backtesting with refit and increasing training size¶

In this strategy, the model is trained before making predictions each time, and all available data up to that point is used in the training process. This differs from standard cross-validation, where the data is randomly distributed between training and validation sets.

Instead of randomizing the data, this backtesting sequentially increases the size of the training set while maintaining the temporal order of the data. By doing this, the model can be tested on progressively larger amounts of historical data, providing a more accurate assessment of its predictive capabilities.

Backtesting with refit and increasing training size (fixed origin).

Note: The arguments needed to achieve this configuration are refit=True and fixed_train_size=False.

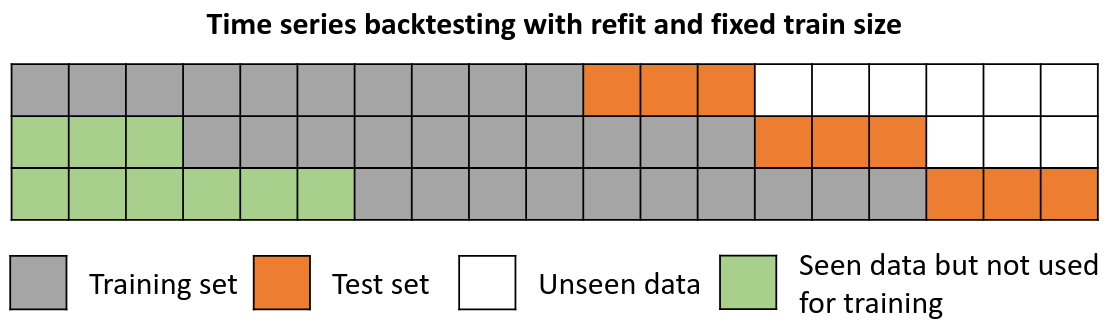

Backtesting with refit and fixed training size¶

In this approach, the model is trained using a fixed window of past observations, and the testing is performed on a rolling basis, where the training window is moved forward in time. The size of the training window is kept constant, allowing for the model to be tested on different sections of the data. This technique is particularly useful when there is a limited amount of data available, or when the data is non-stationary, and the model's performance may vary over time. Is also known as time series cross-validation or walk-forward validation.

Backtesting with refit and fixed training size (rolling origin).

Note: The arguments needed to achieve this configuration are refit=True and fixed_train_size=True.

Backtesting with intermittent refit¶

The model is retrained every iterations of prediction. This method is often used when the frequency of retraining and prediction is different. It can be implemented using either a fixed or rolling origin, providing flexibility in adapting the model to new data.

Tip

This strategy usually achieves a good balance between the computational cost of retraining and avoiding model degradation.

Backtesting with intermittent refit.

Note: The argument needed to achieve this configuration is refit=n, where is an integer. This configuration also allows the use of fixed_train_size.

Backtesting including gap¶

This approach introduces a time gap between the training and test sets, replicating a scenario where predictions cannot be made immediately after the end of the training data.

For example, consider the goal of predicting the 24 hours of day D+1, but the predictions need to be made at 11:00 to allow sufficient flexibility. At 11:00 on day D, the task is to forecast hours [12 - 23] of the same day and hours [0 - 23] of day D+1. Thus, a total of 36 hours into the future must be predicted, with only the last 24 hours to be stored.

Backtesting with refit and gap.

Note: After setting the desired values for refit and fixed_train_size. The argument needed to achieve this configuration is gap=n, where is an integer.

Which strategy should I use?¶

To ensure an accurate evaluation of your model and gain confidence in its predictive performance on new data, it is critical to employ an appropriate backtesting strategy. Factors such as use case characteristics, available computing resources and time intervals between predictions need to be considered to determine which strategy to use. These factors determine when the model should be refitted and the prediction horizon that should be used.

Prediction horizon (

steps): suppose you need to predict the users of an application every Monday for the whole week. In this case, each iteration of backtesting would be a seven-step prediction, representing the seven days of the week.Refit strategy (

refit): Continuing with the example above, at the end of the week you need to decide whether or not to update the model. Training the model with additional data can improve its predictive ability, but it requires more time and computational resources, which may not always be readily available. A reasonable approach is to compare different retrain frequencies and select the one for which the error metric shows a consistent upward trend. This behaviour can be effectively simulated using the backtesting framework.

As an example, backtesting is performed using the data from this skforecast example. The same backtest is run with steps=24 (predict 24 hours) and different refit strategies: False (no re-fitting between predictions), re-fitting every 30 days, every 14 days, every 7 days and True (re-fitting after every prediction). Notice that the significant increase in time does not correspond to a decrease in error.

| refit value | execution time (s) | metric |

|---|---|---|

| False | 1.4 | 262.5 |

| 30 | 4.0 | 263.4 |

| 14 | 6.3 | 262.5 |

| 7 | 11.1 | 261.4 |

| True | 69.1 | 258.3 |

In general, the more closely the backtesting process resembles the actual scenario in which the model is used, the more reliable the estimated metric will be.

Note

Since skforecast 0.9.0, all backtesting and grid search functions have been extended to include the n_jobs argument, allowing multi-process parallelization for improved performance. This applies to all functions of the different model_selection modules.

The benefits of parallelization depend on several factors, including the regressor used, the number of fits to be performed, and the volume of data involved. When the n_jobs parameter is set to 'auto', the level of parallelization is automatically selected based on heuristic rules that aim to choose the best option for each scenario.

For a more detailed look at parallelization, visit Parallelization in skforecast.

Libraries¶

# Libraries

# ==============================================================================

import pandas as pd

import matplotlib.pyplot as plt

from skforecast.datasets import fetch_dataset

from skforecast.ForecasterAutoreg import ForecasterAutoreg

from skforecast.model_selection import backtesting_forecaster

from sklearn.linear_model import Ridge

from sklearn.ensemble import RandomForestRegressor

from sklearn.metrics import mean_squared_error

Data¶

# Download data

# ==============================================================================

data = fetch_dataset(

name="h2o", raw=True, kwargs_read_csv={"names": ["y", "datetime"], "header": 0}

)

# Data preprocessing

# ==============================================================================

data['datetime'] = pd.to_datetime(data['datetime'], format='%Y-%m-%d')

data = data.set_index('datetime')

data = data.asfreq('MS')

data = data[['y']]

data = data.sort_index()

# Train-validation dates

# ==============================================================================

end_train = '2002-01-01 23:59:00'

print(

f"Train dates : {data.index.min()} --- {data.loc[:end_train].index.max()}"

f" (n={len(data.loc[:end_train])})"

)

print(

f"Validation dates : {data.loc[end_train:].index.min()} --- {data.index.max()}"

f" (n={len(data.loc[end_train:])})"

)

# Plot

# ==============================================================================

fig, ax = plt.subplots(figsize=(6, 3))

data.loc[:end_train].plot(ax=ax, label='train')

data.loc[end_train:].plot(ax=ax, label='validation')

ax.legend()

plt.show()

display(data.head(4))

h2o --- Monthly expenditure ($AUD) on corticosteroid drugs that the Australian health system had between 1991 and 2008. Hyndman R (2023). fpp3: Data for Forecasting: Principles and Practice(3rd Edition). http://pkg.robjhyndman.com/fpp3package/,https://github.com/robjhyndman /fpp3package, http://OTexts.com/fpp3. Shape of the dataset: (204, 2) Train dates : 1991-07-01 00:00:00 --- 2002-01-01 00:00:00 (n=127) Validation dates : 2002-02-01 00:00:00 --- 2008-06-01 00:00:00 (n=77)

| y | |

|---|---|

| datetime | |

| 1991-07-01 | 0.429795 |

| 1991-08-01 | 0.400906 |

| 1991-09-01 | 0.432159 |

| 1991-10-01 | 0.492543 |

Backtest¶

An example of a backtesting with refit consists of the following steps:

Train the model using an initial training set, the length of which is specified by

initial_train_size.Once the model is trained, it is used to make predictions for the next 10 steps (

steps=10) in the data. These predictions are saved for later evaluation.As

refitis set toTrue, the size of the training set is increased by adding the lats 10 data points (the previously predicted 10 steps), while the next 10 steps are used as test data.After expanding the training set, the model is retrained using the updated training data and then used to predict the next 10 steps.

Repeat steps 3 and 4 until the entire series has been tested.

By following these steps, you can ensure that the model is evaluated on multiple sets of test data, thereby providing a more accurate assessment of its predictive power.

# Backtesting forecaster

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = RandomForestRegressor(random_state=123),

lags = 15

)

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = 'mean_squared_error',

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 0,

allow_incomplete_fold = True,

refit = True,

n_jobs = 'auto',

verbose = True,

show_progress = True

)

Information of backtesting process

----------------------------------

Number of observations used for initial training: 127

Number of observations used for backtesting: 77

Number of folds: 8

Number of steps per fold: 10

Number of steps to exclude from the end of each train set before test (gap): 0

Last fold only includes 7 observations.

Fold: 0

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2002-02-01 00:00:00 -- 2002-11-01 00:00:00 (n=10)

Fold: 1

Training: 1991-07-01 00:00:00 -- 2002-11-01 00:00:00 (n=137)

Validation: 2002-12-01 00:00:00 -- 2003-09-01 00:00:00 (n=10)

Fold: 2

Training: 1991-07-01 00:00:00 -- 2003-09-01 00:00:00 (n=147)

Validation: 2003-10-01 00:00:00 -- 2004-07-01 00:00:00 (n=10)

Fold: 3

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2004-08-01 00:00:00 -- 2005-05-01 00:00:00 (n=10)

Fold: 4

Training: 1991-07-01 00:00:00 -- 2005-05-01 00:00:00 (n=167)

Validation: 2005-06-01 00:00:00 -- 2006-03-01 00:00:00 (n=10)

Fold: 5

Training: 1991-07-01 00:00:00 -- 2006-03-01 00:00:00 (n=177)

Validation: 2006-04-01 00:00:00 -- 2007-01-01 00:00:00 (n=10)

Fold: 6

Training: 1991-07-01 00:00:00 -- 2007-01-01 00:00:00 (n=187)

Validation: 2007-02-01 00:00:00 -- 2007-11-01 00:00:00 (n=10)

Fold: 7

Training: 1991-07-01 00:00:00 -- 2007-11-01 00:00:00 (n=197)

Validation: 2007-12-01 00:00:00 -- 2008-06-01 00:00:00 (n=7)

0%| | 0/8 [00:00<?, ?it/s]

# Backtest error

# ==============================================================================

print(f"Backtest error: {metric}")

predictions.head(4)

Backtest error: 0.00818535931502708

| pred | |

|---|---|

| 2002-02-01 | 0.594506 |

| 2002-03-01 | 0.785886 |

| 2002-04-01 | 0.698925 |

| 2002-05-01 | 0.790560 |

# Plot predictions

# ==============================================================================

fig, ax = plt.subplots(figsize=(6, 3))

data.loc[end_train:, 'y'].plot(ax=ax)

predictions.plot(ax=ax)

ax.legend()

plt.show();

Backtesting intermittent refit¶

The same backtesting as above is repeated, but this time with refit = 3. The training of the model is done every 3 folds instead of every fold.

Note

With an intermittent refit, the model is trained every refit * steps observations. In this case, 3 * 10 = 30 observations. This can be easily observed in the verbose logs.

# Backtesting with intermittent refit

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = RandomForestRegressor(random_state=123),

lags = 15

)

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = 'mean_squared_error',

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

allow_incomplete_fold = True,

refit = 3,

verbose = True,

show_progress = True

)

Information of backtesting process

----------------------------------

Number of observations used for initial training: 127

Number of observations used for backtesting: 77

Number of folds: 8

Number of steps per fold: 10

Number of steps to exclude from the end of each train set before test (gap): 0

Last fold only includes 7 observations.

Fold: 0

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2002-02-01 00:00:00 -- 2002-11-01 00:00:00 (n=10)

Fold: 1

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2002-12-01 00:00:00 -- 2003-09-01 00:00:00 (n=10)

Fold: 2

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2003-10-01 00:00:00 -- 2004-07-01 00:00:00 (n=10)

Fold: 3

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2004-08-01 00:00:00 -- 2005-05-01 00:00:00 (n=10)

Fold: 4

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2005-06-01 00:00:00 -- 2006-03-01 00:00:00 (n=10)

Fold: 5

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2006-04-01 00:00:00 -- 2007-01-01 00:00:00 (n=10)

Fold: 6

Training: 1991-07-01 00:00:00 -- 2007-01-01 00:00:00 (n=187)

Validation: 2007-02-01 00:00:00 -- 2007-11-01 00:00:00 (n=10)

Fold: 7

Training: 1991-07-01 00:00:00 -- 2007-01-01 00:00:00 (n=187)

Validation: 2007-12-01 00:00:00 -- 2008-06-01 00:00:00 (n=7)

0%| | 0/8 [00:00<?, ?it/s]

# Backtest error

# ==============================================================================

print(f"Backtest error: {metric}")

predictions.head(4)

Backtest error: 0.008352839337768609

| pred | |

|---|---|

| 2002-02-01 | 0.594506 |

| 2002-03-01 | 0.785886 |

| 2002-04-01 | 0.698925 |

| 2002-05-01 | 0.790560 |

Backtesting with gap¶

The gap size can be adjusted with the gap argument. In addition, the allow_incomplete_fold parameter allows the last fold to be excluded from the analysis if it doesn't have the same size as the required number of steps.

These arguments can be used in conjunction with either refit set to True or False, depending on the needs and objectives of the use case.

Note

In this example, although only the last 10 predictions (steps) are stored for model evaluation, the total number of predicted steps in each fold is 15 (steps + gap).

# Backtesting forecaster

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = RandomForestRegressor(random_state=123),

lags = 15

)

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = 'mean_squared_error',

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 5,

allow_incomplete_fold = False,

refit = True,

verbose = True,

show_progress = True

)

Information of backtesting process

----------------------------------

Number of observations used for initial training: 127

Number of observations used for backtesting: 77

Number of folds: 7

Number of steps per fold: 10

Number of steps to exclude from the end of each train set before test (gap): 5

Last fold has been excluded because it was incomplete.

Fold: 0

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2002-07-01 00:00:00 -- 2003-04-01 00:00:00 (n=10)

Fold: 1

Training: 1991-07-01 00:00:00 -- 2002-11-01 00:00:00 (n=137)

Validation: 2003-05-01 00:00:00 -- 2004-02-01 00:00:00 (n=10)

Fold: 2

Training: 1991-07-01 00:00:00 -- 2003-09-01 00:00:00 (n=147)

Validation: 2004-03-01 00:00:00 -- 2004-12-01 00:00:00 (n=10)

Fold: 3

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2005-01-01 00:00:00 -- 2005-10-01 00:00:00 (n=10)

Fold: 4

Training: 1991-07-01 00:00:00 -- 2005-05-01 00:00:00 (n=167)

Validation: 2005-11-01 00:00:00 -- 2006-08-01 00:00:00 (n=10)

Fold: 5

Training: 1991-07-01 00:00:00 -- 2006-03-01 00:00:00 (n=177)

Validation: 2006-09-01 00:00:00 -- 2007-06-01 00:00:00 (n=10)

Fold: 6

Training: 1991-07-01 00:00:00 -- 2007-01-01 00:00:00 (n=187)

Validation: 2007-07-01 00:00:00 -- 2008-04-01 00:00:00 (n=10)

0%| | 0/7 [00:00<?, ?it/s]

# Backtest error

# ==============================================================================

print(f"Backtest error: {metric}")

predictions.head(4)

Backtest error: 0.011194317866594718

| pred | |

|---|---|

| 2002-07-01 | 0.870897 |

| 2002-08-01 | 0.920207 |

| 2002-09-01 | 0.942503 |

| 2002-10-01 | 1.022695 |

Backtesting with prediction intervals¶

Backtesting can be used not only to obtain point estimate predictions but also to obtain prediction intervals. Prediction intervals provide a range of values within which the actual values are expected to fall with a certain level of confidence. By estimating prediction intervals during backtesting, one can get a better understanding of the uncertainty associated with your model's predictions. This information can be used to assess the reliability of the model's predictions and to make more informed decisions. To learn more about probabilistic forecasting, visit Probabilistic forecasting.

# Backtesting forecaster with prediction intervals

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = Ridge(random_state=123),

lags = 15

)

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = 'mean_squared_error',

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 0,

allow_incomplete_fold = True,

refit = True,

interval = [5, 95],

n_boot = 500,

verbose = True,

show_progress = True

)

Information of backtesting process

----------------------------------

Number of observations used for initial training: 127

Number of observations used for backtesting: 77

Number of folds: 8

Number of steps per fold: 10

Number of steps to exclude from the end of each train set before test (gap): 0

Last fold only includes 7 observations.

Fold: 0

Training: 1991-07-01 00:00:00 -- 2002-01-01 00:00:00 (n=127)

Validation: 2002-02-01 00:00:00 -- 2002-11-01 00:00:00 (n=10)

Fold: 1

Training: 1991-07-01 00:00:00 -- 2002-11-01 00:00:00 (n=137)

Validation: 2002-12-01 00:00:00 -- 2003-09-01 00:00:00 (n=10)

Fold: 2

Training: 1991-07-01 00:00:00 -- 2003-09-01 00:00:00 (n=147)

Validation: 2003-10-01 00:00:00 -- 2004-07-01 00:00:00 (n=10)

Fold: 3

Training: 1991-07-01 00:00:00 -- 2004-07-01 00:00:00 (n=157)

Validation: 2004-08-01 00:00:00 -- 2005-05-01 00:00:00 (n=10)

Fold: 4

Training: 1991-07-01 00:00:00 -- 2005-05-01 00:00:00 (n=167)

Validation: 2005-06-01 00:00:00 -- 2006-03-01 00:00:00 (n=10)

Fold: 5

Training: 1991-07-01 00:00:00 -- 2006-03-01 00:00:00 (n=177)

Validation: 2006-04-01 00:00:00 -- 2007-01-01 00:00:00 (n=10)

Fold: 6

Training: 1991-07-01 00:00:00 -- 2007-01-01 00:00:00 (n=187)

Validation: 2007-02-01 00:00:00 -- 2007-11-01 00:00:00 (n=10)

Fold: 7

Training: 1991-07-01 00:00:00 -- 2007-11-01 00:00:00 (n=197)

Validation: 2007-12-01 00:00:00 -- 2008-06-01 00:00:00 (n=7)

0%| | 0/8 [00:00<?, ?it/s]

# Interval predictions

# ==============================================================================

predictions.head()

| pred | lower_bound | upper_bound | |

|---|---|---|---|

| 2002-02-01 | 0.703579 | 0.607557 | 0.811388 |

| 2002-03-01 | 0.673522 | 0.570660 | 0.787793 |

| 2002-04-01 | 0.698319 | 0.593406 | 0.827166 |

| 2002-05-01 | 0.703042 | 0.604403 | 0.824053 |

| 2002-06-01 | 0.733776 | 0.632228 | 0.842451 |

# Plot prediction intervals

# ==============================================================================

fig, ax = plt.subplots(figsize=(6, 3))

data.loc[end_train:, 'y'].plot(ax=ax, label='test')

predictions['pred'].plot(ax=ax, label='predictions')

ax.fill_between(

predictions.index,

predictions['lower_bound'],

predictions['upper_bound'],

color = 'red',

alpha = 0.2,

label = 'prediction interval'

)

ax.legend();

Backtesting with exogenous variables¶

All the backtesting strategies discussed in this document can also be applied when incorporating exogenous variables in the forecasting model.

Exogenous variables are additional independent variables that can impact the value of the target variable being forecasted. These variables can provide valuable information to the model and improve its forecasting accuracy.

# Download data

# ==============================================================================

data = fetch_dataset(name='h2o_exog', raw=False)

data.index.name = 'datetime'

h2o_exog -------- Monthly expenditure ($AUD) on corticosteroid drugs that the Australian health system had between 1991 and 2008. Two additional variables (exog_1, exog_2) are simulated. Hyndman R (2023). fpp3: Data for Forecasting: Principles and Practice (3rd Edition). http://pkg.robjhyndman.com/fpp3package/, https://github.com/robjhyndman/fpp3package, http://OTexts.com/fpp3. Shape of the dataset: (195, 3)

# Train-validation dates

# ==============================================================================

end_train = '2002-01-01 23:59:00'

print(

f"Train dates : {data.index.min()} --- {data.loc[:end_train].index.max()}"

f" (n={len(data.loc[:end_train])})"

)

print(

f"Validation dates : {data.loc[end_train:].index.min()} --- {data.index.max()}"

f" (n={len(data.loc[end_train:])})"

)

# Plot

# ==============================================================================

fig, ax=plt.subplots(figsize=(6, 3))

data.plot(ax=ax);

Train dates : 1992-04-01 00:00:00 --- 2002-01-01 00:00:00 (n=118) Validation dates : 2002-02-01 00:00:00 --- 2008-06-01 00:00:00 (n=77)

# Backtest forecaster exogenous variables

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = RandomForestRegressor(random_state=123),

lags = 15

)

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

exog = data[['exog_1', 'exog_2']],

steps = 10,

metric = 'mean_squared_error',

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 0,

allow_incomplete_fold = True,

refit = True,

verbose = True,

show_progress = True

)

Information of backtesting process

----------------------------------

Number of observations used for initial training: 118

Number of observations used for backtesting: 77

Number of folds: 8

Number of steps per fold: 10

Number of steps to exclude from the end of each train set before test (gap): 0

Last fold only includes 7 observations.

Fold: 0

Training: 1992-04-01 00:00:00 -- 2002-01-01 00:00:00 (n=118)

Validation: 2002-02-01 00:00:00 -- 2002-11-01 00:00:00 (n=10)

Fold: 1

Training: 1992-04-01 00:00:00 -- 2002-11-01 00:00:00 (n=128)

Validation: 2002-12-01 00:00:00 -- 2003-09-01 00:00:00 (n=10)

Fold: 2

Training: 1992-04-01 00:00:00 -- 2003-09-01 00:00:00 (n=138)

Validation: 2003-10-01 00:00:00 -- 2004-07-01 00:00:00 (n=10)

Fold: 3

Training: 1992-04-01 00:00:00 -- 2004-07-01 00:00:00 (n=148)

Validation: 2004-08-01 00:00:00 -- 2005-05-01 00:00:00 (n=10)

Fold: 4

Training: 1992-04-01 00:00:00 -- 2005-05-01 00:00:00 (n=158)

Validation: 2005-06-01 00:00:00 -- 2006-03-01 00:00:00 (n=10)

Fold: 5

Training: 1992-04-01 00:00:00 -- 2006-03-01 00:00:00 (n=168)

Validation: 2006-04-01 00:00:00 -- 2007-01-01 00:00:00 (n=10)

Fold: 6

Training: 1992-04-01 00:00:00 -- 2007-01-01 00:00:00 (n=178)

Validation: 2007-02-01 00:00:00 -- 2007-11-01 00:00:00 (n=10)

Fold: 7

Training: 1992-04-01 00:00:00 -- 2007-11-01 00:00:00 (n=188)

Validation: 2007-12-01 00:00:00 -- 2008-06-01 00:00:00 (n=7)

0%| | 0/8 [00:00<?, ?it/s]

# Backtest error

# ==============================================================================

print(f"Backtest error with exogenous variables: {metric}")

Backtest error with exogenous variables: 0.007800037462113706

# Plot predictions

# ==============================================================================

fig, ax = plt.subplots(figsize=(6, 3))

data.loc[end_train:].plot(ax=ax)

predictions.plot(ax=ax)

ax.legend(loc="upper left")

plt.show();

Backtesting with custom metric¶

In addition to the commonly used metrics such as mean_squared_error, mean_absolute_error, and mean_absolute_percentage_error, users have the flexibility to define their own custom metric function, provided that it includes the arguments y_true (the true values of the series) and y_pred (the predicted values), and returns a numeric value (either a float or an int).

This customizability enables users to evaluate the model's predictive performance in a wide range of scenarios, such as considering only certain months, days, non holiday; or focusing only on the last step of the predicted horizon.

To illustrate this, consider the following example: a 12-month horizon is forecasted, but the interest metric is calculated by considering only the last three months of each year. This is achieved by defining a custom metric function that takes into account only the relevant months, which is then passed as an argument to the backtesting function.

# Backtesting with custom metric

# ==============================================================================

def custom_metric(y_true, y_pred):

"""

Calculate the mean squared error using only the predicted values of the last

3 months of the year.

"""

mask = y_true.index.month.isin([10, 11, 12])

metric = mean_squared_error(y_true[mask], y_pred[mask])

return metric

metric, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = custom_metric,

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 0,

allow_incomplete_fold = True,

refit = True,

verbose = False,

show_progress = True

)

print(f"Backtest error custom metric: {metric}")

0%| | 0/8 [00:00<?, ?it/s]

Backtest error custom metric: 0.005482666107945366

Backtesting with multiple metrics¶

The backtesting_forecaster function provides a convenient way to estimate multiple metrics simultaneously by accepting a list of metrics as an input argument. This list can include any combination of built-in metrics, such as mean_squared_error, mean_absolute_error, and mean_absolute_percentage_error, as well as user-defined custom metrics.

By specifying multiple metrics, users can obtain a more comprehensive evaluation of the model's predictive performance, which can help in selecting the best model for a particular task. Additionally, the ability to include custom metrics allows users to tailor the evaluation to specific use cases and domain-specific requirements.

# Backtesting with multiple metric

# ==============================================================================

multiple_metrics = ['mean_squared_error', 'mean_absolute_error', custom_metric]

metrics, predictions = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 10,

metric = multiple_metrics,

initial_train_size = len(data.loc[:end_train]),

fixed_train_size = False,

gap = 0,

allow_incomplete_fold = True,

refit = True,

verbose = False,

show_progress = True

)

print(f"Backtest error metrics: {metrics}")

0%| | 0/8 [00:00<?, ?it/s]

Backtest error metrics: [0.00804575658744146, 0.06502216041298702, 0.005482666107945366]

Backtesting on training data¶

While the main focus of creating forecasting models is predicting future values, it's also useful to evaluate whether the model is learning from the training data. Predictions on the training data can help with this evaluation.

To obtain predictions on the training data,the forecaster must first be fitted using the training dataset. Then, backtesting can be performed using backtesting_forecaster and specifying the arguments initial_train_size=None and refit=False. This configuration enables backtesting on the same data that was used to train the model.

# Create and fit forecaster

# ==============================================================================

forecaster = ForecasterAutoreg(

regressor = RandomForestRegressor(random_state=123),

lags = 15

)

forecaster.fit(y=data['y'])

# Backtesting on training data

# ==============================================================================

metric, predictions_training = backtesting_forecaster(

forecaster = forecaster,

y = data['y'],

steps = 1,

metric = 'mean_squared_error',

initial_train_size = None,

refit = False,

verbose = False,

show_progress = True

)

print(f"Backtest training error: {metric}")

0%| | 0/180 [00:00<?, ?it/s]

Backtest training error: 0.0005647902993476632

# Training predictions

# ==============================================================================

predictions_training.head(4)

| pred | |

|---|---|

| 1993-07-01 | 0.515375 |

| 1993-08-01 | 0.558055 |

| 1993-09-01 | 0.597601 |

| 1993-10-01 | 0.618857 |

It is important to note that the first 15 observations are excluded from the predictions since they are required to generate the lags that serve as predictors in the model.

# Plot training predictions

# ==============================================================================

fig, ax = plt.subplots(figsize=(6, 3))

data['y'].plot(ax=ax)

predictions_training.plot(ax=ax)

ax.set_title("Backtesting on training data")

ax.legend()

plt.show();